Chimeric antigen receptor T-cell (CAR-T) therapies promise to transform treatment of many cancers but have been slow to gain wide use. We argue that the CAR-Ts’ high costs ought to be thought of in light of the many years of life they can add over standard therapy. Even amortizing CAR-T costs over two years puts them in a similar cost-benefit zone as many other highly innovative cancer therapies. Pay-for-performance schemes, such as some being used for CAR-Ts in Europe to reduce payer risk, offer another path to more acceptable costs.

Marketed CAR-Ts are indicated only for hematological malignancies, but there are many developmental programs targeting solid tumors. Moreover, efforts are under way to extend the technology beyond the current autologous approach to include allogeneic solutions, which could ease the cost and complexity of treating with CAR-T therapies.

In this post we analyze the commercial outlook for CAR-Ts, given their unique characteristics, especially:

dramatic clinical improvement (near-cures in approximately 40% of treated patients) and

very high prices (typically north of $400,000 to treat a single patient)

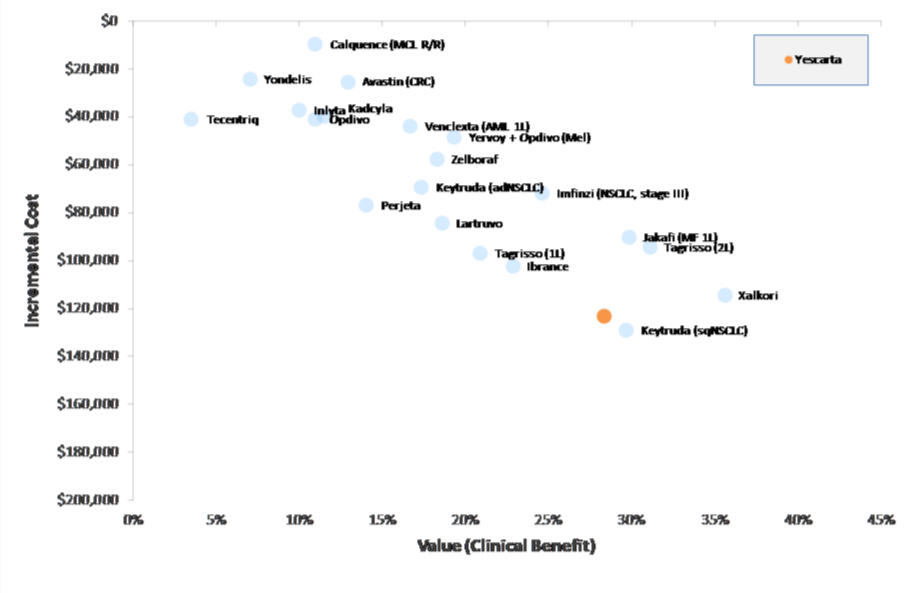

We have analyzed several CAR-T therapies through the lens of our Disease Target Assessment (DTA) framework, which provides (1) an objective and comparable basis for quantifying the magnitude of clinical improvement offered by a therapy, and (2) a measure of clinical benefit compared to price – is the benefit/cost ratio similar to other new oncology drugs that have achieved good market access?

Yescarta

Yescarta (axicabtagene ciloleucel) won its first FDA approval in 2017 and can be considered a moderate commercial success. Its clinical innovation, notably its efficacy, puts it in what has historically been breakthrough territory by our measures. In third-line-plus diffuse large B cell lymphoma (3L+ DLBCL), Yescarta boosted median overall survival to 25.8 months from 6.3 months for Rituxan regimens, with similar improvements in progression-free survival and response rates. Importantly, five-year survival with Yescarta was 42.6%--reflecting a fat tail to the survival curve.

Entering these results and other clinical information in our framework puts Yescarta’s clinical innovation over the Rituxan regimen as 21.5%. This figure is well above the 10% threshold that we observe for new drugs that achieve dominant patient share. Yescarta clearly delivers substantial clinical improvement, on par with other commercially successful new drugs. Yescarta shows nearly identical clinical innovation in the newer 2L+ DLBCL population, suggesting strong share potential in that patient group.

Benefit vs. Cost

To address the question of how a drug’s price affects its outlook, our techniques measure the ratio of “Clinical Benefit” vs. cost; through empirical observation we have shown there is a clear benefit/cost relationship among oncology drugs that have achieved favorable market access (see figure below). Priced upwards of $400K, Yescarta is much more expensive than Rituxan regimens in DLBCL, which average ~$20K annually. CAR-Ts incur substantial ancillary costs for apheresis, bridging therapy, conditioning therapy, infusion and post-infusion, along with hospitalization, ICU stays, and ER visits. Patients with life-threatening adverse events such as high-grade cytokine release syndrome (CRS) incur higher than average costs. All told, the total direct costs of CAR-T therapy can reach ~$650K in DLBCL. In contrast to more conventional drug therapies, all of that cost is incurred up-front.

Because costs are front-loaded while the benefits are durable, we believe these costs should be amortized. We consider a two-year horizon reasonable (i.e., cutting first-year costs in half). Using that assumption, Yescarta’s benefit to cost ratio in 3L+ DLBCL is in line with other novel oncology therapies that have achieved good market access. This is also true for Yescarta in the 2L+ DLBCL population).

Other Approved CAR-Ts

BMS’s Breyanzi has similar clinical characteristics to Yescarta’s in both 3L+ and 2L+ DLBCL, and although launched several years after Yescarta, it is seeing reasonably good uptake. Still more recent is Janssen’s Carvykti in 5L+ multiple myeloma; this agent has even more impressive clinical innovation (40%), and also offers a good clinical benefit to price ratio. Given those results, we think Carvykti will be successful as it gains approvals in earlier lines of therapy.

Barriers to Use

Factors aside from clinical benefit and price also affect CAR-T share. CAR-Ts are only available at authorized treatment centers (ATCs). While there are over 110 ATCs in the United States, their uneven geographical distribution poses challenges. The elapsed time between sampling a patient’s T-cells and reinfusing treated cells limits CAR-T use to patients who have enough time to benefit from it. Ancillary costs are high and may face uncertain reimbursement.

Key Questions Affecting the Outlook for a New CAR-T Program

Equinox conducted this analysis to investigate the extent to which our analytical tools can help development teams anticipate the commercial potential for CAR-T (and other regenerative medicine therapies) programs. Our preliminary conclusion is that the same metrics we have applied for years to more traditional oncology therapies seem to provide similar insight even in the special case of cell therapies. Evidence so far confirms that the level of clinical improvement and its relationship to price remain important factors.